Is this conversation (or a variation of it) familiar?

Jimmy walks into his accountant’s office and says, “I have to pay for my daughter’s college but I really don’t want to sell my stocks and pay tax on the large gains. How can I get around paying the capital gains tax?”

Sally, his accountant, ponders his question for a bit, and responds with, “Well, there are a few options for avoiding tax on your stock winners—gifting, planning, and dying.”

Jimmy leans in and says, “Tell me more.”

Sally describes the tax benefits of gifting appreciated stocks to charity. She then proceeds to explain how planning ahead can help folks like Jimmy pay taxes in the years that are most advantageous to him.

Not one to give up easily, Jimmy asks, “And the dying option?”

Without pause, Sally quips, “When you die your heirs get an automatic step up in their cost basis—meaning the stock’s cost basis resets to the current market price so there isn’t a gain from a tax perspective…it’s the classic tax-avoidance maneuver!”

Now that puts an interesting twist on Ben Franklin’s famous saying,

…and it’s also probably not the answer Jimmy sought!

But it brings forth a very common problem for many investors: How can you minimize the tax hit on your investment portfolio? And taking it a step further for retirees or those nearing retirement, how can you reduce taxes in retirement from all sources of income?

Alas, we’re here to help. Our financial planning team confronts these quandaries every day to help retirees structure their wealth in a tax-efficient manner. Because if you don’t plan for the erosion from taxes, you can lose nearly 40% of your money in some cases, especially after considering the impact of state-level taxes.

In this report, we answer three popular questions for you:

- What taxes do I have to pay, and at what rate?

- Which type of account maximizes after-tax income and growth?

- What strategies should I consider now—and later—to reduce taxes for myself and my heirs?

To print this report or save it as a PDF, click here.

Before we begin, we want to note that while we can offer insights on tax efficiency and discuss tax considerations in a general way, Motley Fool Wealth Management does not (and is not permitted to) provide tax or legal advice. Remember, the discussion of tax strategies in this report is intended for educational purposes only and should not be relied upon as personalized tax or financial planning advice.

If you need such advice, please consult with your own tax and legal professionals before making any decisions.

With all that said, let’s dig in!

Taxes, Taxes, Taxes

Tax-Efficient Wealth Planning

We think individuals have some options when it comes to how much and when they pay their taxes. In other words, while we cannot always eliminate taxes completely, there are several legal ways to structure income to mitigate your tax bill. When considering tax-mitigation strategies, we look at two sides of the tax equation—income and deductions. We’re guided by two broad principles:

While everyone’s situation is different and these are highly personalized planning decisions, we adhere to six rules of thumb to shrink your general tax burden.

Rule 1

Pay tax in stages of life when your income is relatively low, and therefore your tax rate is also low, and defer tax in stages of your life when your income is relatively high.

Rule 2

Understand the value of the standard deduction. From a tax perspective, accumulating deductions like medical expenses, mortgage interest, and charitable giving is only helpful if you are already over the standard deduction threshold.

Rule 3

Consider the timing and manner of charitable contributions to optimize your tax deduction AND your impact.

Rule 4

Gift cash as a last resort.

Rule 5

Consider a Roth conversion if you want to give to your heirs, but not to charity. (Charities are tax-exempt so you should gift pre-tax money!)

Rule 6

Be aware of how your different income streams have unique tax efficiences. For example, self-employment and real estate earnings are taxed as ordinary income, which allows you the opportunity to deduct expenses against it prior to taxation.

Applying these general tenets to the accumulation phase

We believe if you're early in your career when your income—and tax rate—is usually comparatively low, you should save in this order:

- First, contribute up to the match amount in an employer-sponsored retirement plan to receive the “free” money from your employer.

- Then, add the maximum to a Roth IRA, not a traditional IRA. Why a Roth? Because while the money put into a Roth is after-tax, at this stage, you’ll likely have a lower tax rate than later in your career. All withdrawals from a Roth are tax-free and don’t count toward income.

This is beneficial in retirement for several reasons, which we will discuss later, but two major advantages are that withdrawals 1) don’t count as income, so it keeps your tax rate low, and 2) won’t raise your Medicare premiums.

And if you’re in the middle or end of your career—near your peak earning potential— defer income and push taxes to the future. At this stage, max out your pre-tax contributions to your employer-sponsored retirement plan. Also, think about tax deductions. For example, if you want to give to a charity, consider bunching your gifts instead of giving in a steady stream to maximize your deductions.

Holding on to more of your money in the spend-down phase

At the point in your life when you can take advantage of the fruits of your labor—like retirement—you’re probably in the spend-down phase. This stage can look different for everyone. For instance, you may want to create a budget so that you use every last penny before you pass away. Or you may want to touch only interest and keep the principal in your coffers for charity and your heirs into perpetuity. Most people tend to fall somewhere in the middle of this spectrum.

What are the typical sources of income in this phase?

Not all retirement income is equal. Some you’re required to take. Others carry tax consequences. So it’s important to know how to structure the order of your retirement income.

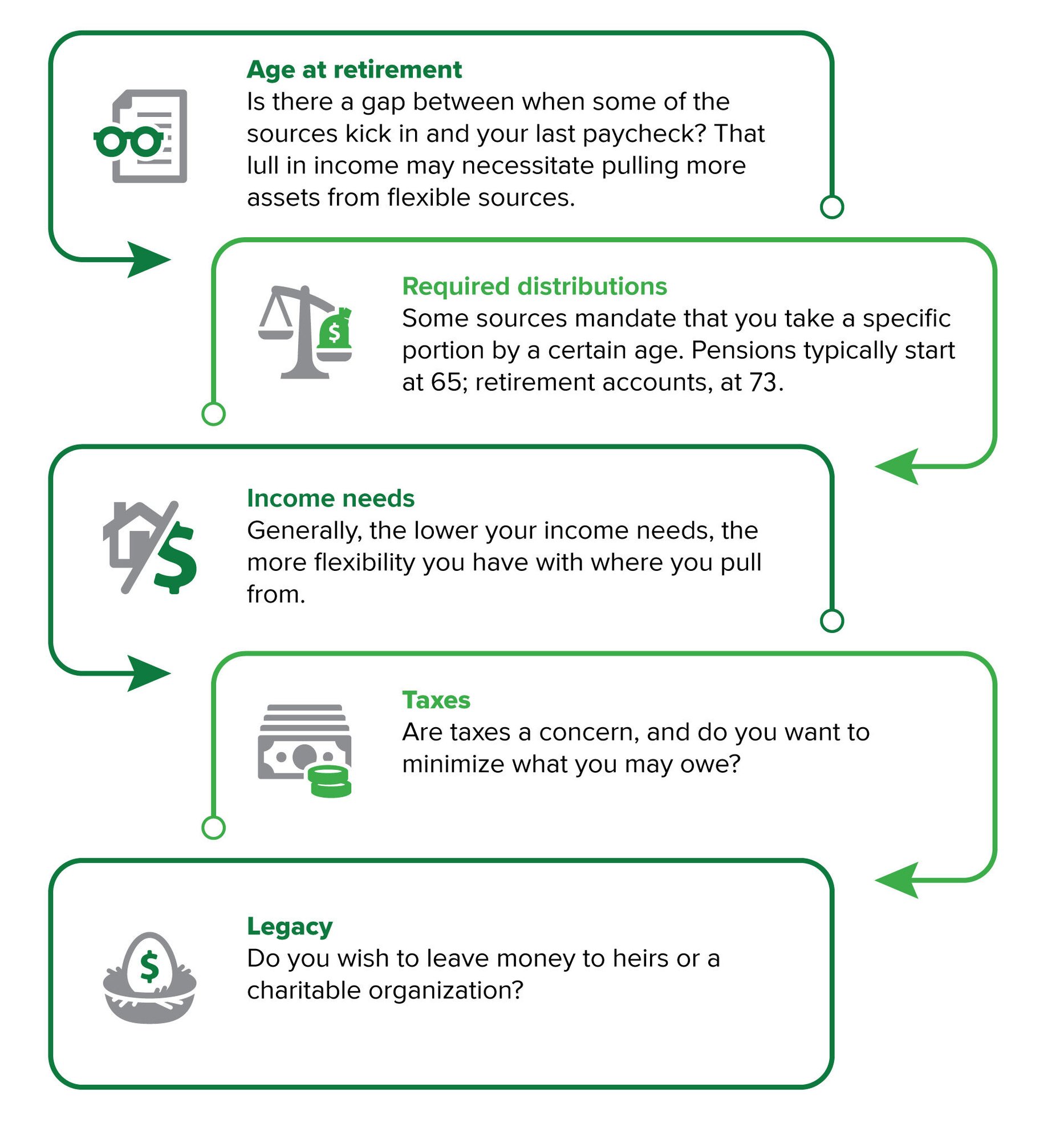

How do you know which income source to take, and at what time? The answer depends on five factors:

These five factors are a starting point to determine how much flexibility you can take on. Unless you need the income right now, here are a few sample strategies to illustrate the kind of decisions you could make if you want more flexibility and tax efficiency:

- Delay Social Security: Even though you can access it at age 62, wait to receive it. Your future monthly benefits increase 8% every year you wait from full retirement age (age 66 or 67) until 70.4

- Avoid required minimum distributions (RMDs): Convert prior to age 73 or gift them via a qualified charitable distribution. We’ll talk more about these options later.

- Cash out your pension: Consider a lump sum payout. Reinvest it in an IRA to control your income flow. You’ll still need to take annual RMDs eventually, but there may be a Roth conversion option if you don’t need them.

- Get rid of your annuities: Sell on the secondary market. Convert your annuity from a fixed-income stream to a lump sum cash option. But, beware: You won’t receive the full cash value—it’s usually discounted 10%–20%, so consult with your annuity professional.

Where does cash fit in?

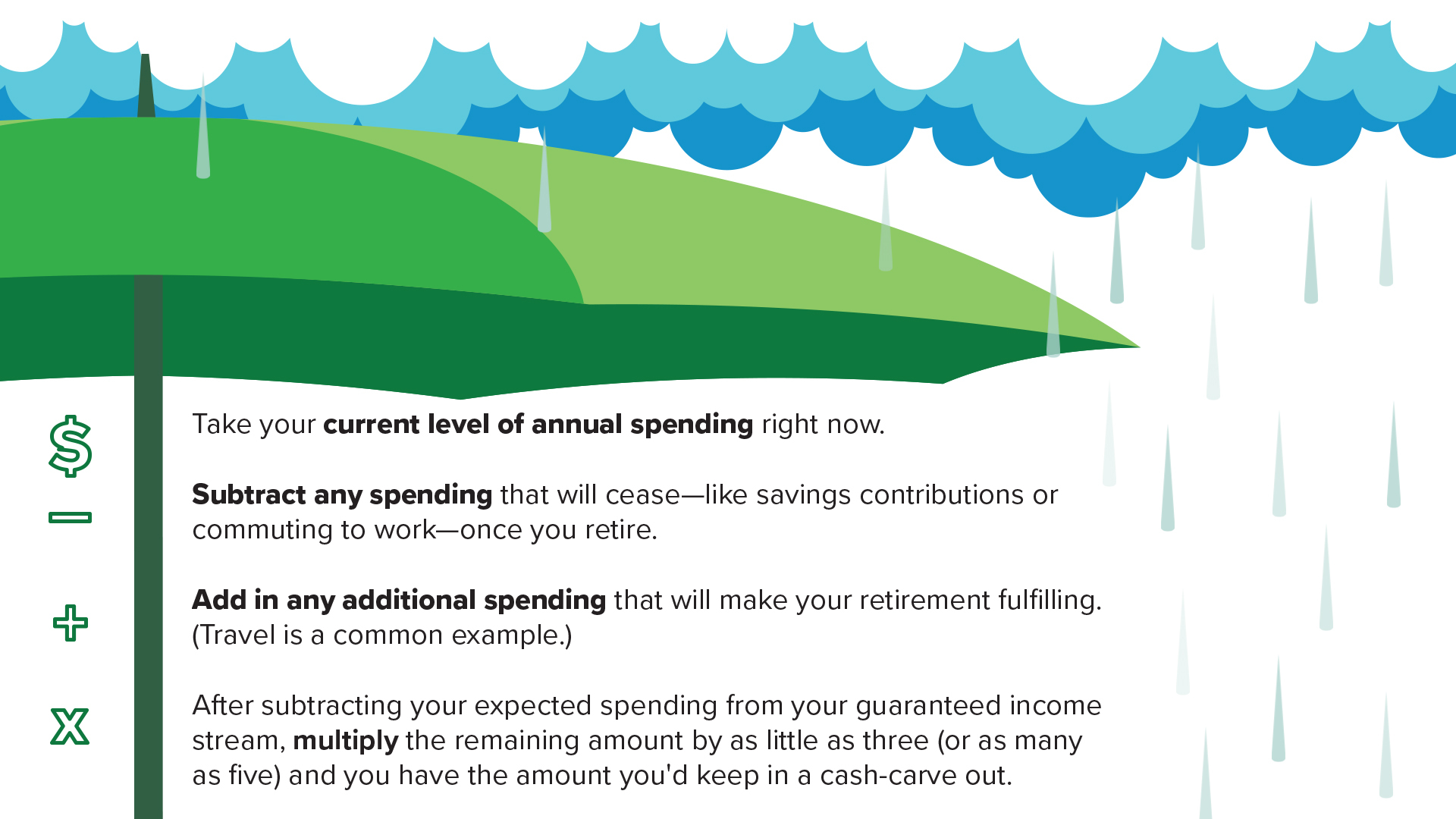

We recommend setting aside three to five years’ worth of savings in a liquid account (money market or short-term government bonds) so that if the stock market drops, you don’t have to worry about your near-term income needs or be forced to sell stocks at fire-sale prices.

Calculating your “cash carve-out” takes a little work, but here’s a way to arrive at a number that may be appropriate for your needs and goals.

Start by considering your income streams. Determine what is guaranteed or reliable income, like a pension or Social Security. Follow the steps below to determine how much cash you need in excess of this reliable, stable income.

For example, if your spending budget is $100K per year, and you receive $60K in pension income, then your cash carve-out per year should cover the remaining $40K. To keep five years’ worth in a rainy day fund, you would need $200K ($40K x 5 years).

Okay, now that we’ve set the stage, let’s dive into our nine savvy tax moves for retirement. We break these into two categories: 1. Getting a “tax bargain” on your income and 2. Getting a “bang for your buck” through deductions, credits, and legacy planning.

| 9 Savvy Tax Moves for Retirement | |||

|---|---|---|---|

| Tax Bargain on Income | Bang for your Buck | ||

| 02Income Tax on Earnings & RMDs | 03Tax on Investment Income | 04Deductions and Credits | 05Legacy Planning |

| Move #1 Time, eliminate & distribute RMDs |

Move #2 Avoid short-term capital gains |

Move #4 Bunch cash gifts |

Move #7 Choose account types |

| Move #3 Match gains with losses |

Move #5 Give appreciated securities |

Move #8 Shield wealth |

|

| Move #6 Combinations |

Move #9 Two-for-one |

||

Income Tax on Earnings and RMDs

Which retirement income is taxed?

The answer is simple: Almost all of it!

Social Security

The federal government taxes up to 85% of your Social Security benefit each year. The taxable amount depends on your combined income, which you can determine by taking your adjusted gross income (AGI) plus non-taxed (tax-exempt) interest income and half of your Social Security benefits.

The taxable amount of Social Security based on your combined income is:

| Individual | Married filing jointly | |

|---|---|---|

| 0% | Up to $25,000 | Up to $32,000 |

| Up to 50% | $25,000 - $34,000 | $32,000 - $44,000 |

| Up to 85% | more than $34,000 | more than $44,000 |

Source: Social Security Administration, accessed May 27, 2025

For example, if your AGI is $10,000, you have no non-taxed interest and receive $50,000 in Social Security, then your combined income is:

$10,000 + $0 + $25,000 (i.e. ½ of $50,000) = $35,000

So as an individual, you will be taxed on 85% of your Social Security, or:

85% x $50,000 = $42,500

In addition to the federal tax, some states also tax Social Security.

Other Retirement Accounts

The most common types of retirement accounts are pensions, 401(k)s or 403(b)s, and traditional IRAs. Since these accounts are considered tax-deferred savings vehicles, you must pay tax when you receive distributions.

Again, the federal government taxes income from tax-deferred accounts—but only when you withdraw the money or take a required distribution—at the same rate as income from an employer (your ordinary income tax rate).

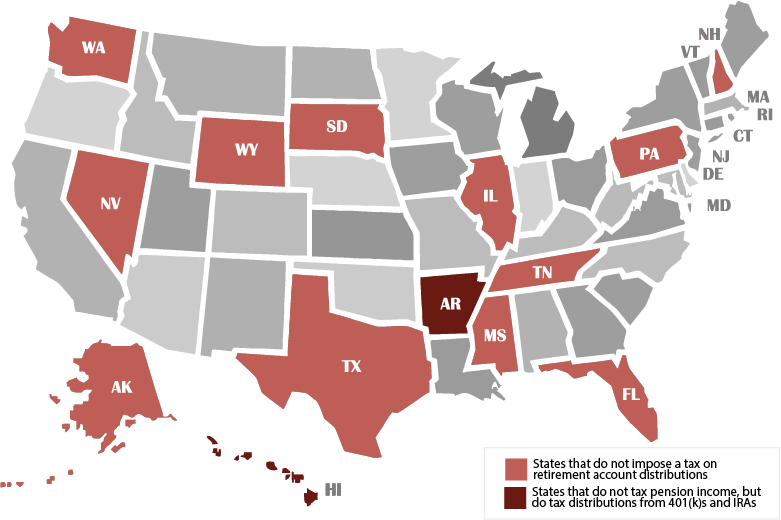

And similar to Social Security, states tax income from retirement accounts too. Almost every state imposes a tax on retirement account distributions. The exceptions are Alaska, Florida, Illinois, Iowa, Mississippi, Nevada, New Hampshire, Pennsylvania, South Dakota, Tennessee, Texas, Washington, and Wyoming. Two other states—Hawaii and Alabama—do not tax pension income, but do tax distributions from 401(k)s and IRAs.

Savvy Tax Move #1

Time, eliminate, & distribute your RMDs

Time your RMDs and other income

The IRS doesn’t care when or how often you take distributions to satisfy your RMDs—as long as you withdraw the appropriate amount by Dec. 31 each year. There’s one exception: You can wait to take your first distribution until April 1 of your 74th year. This is important because if you have a large income event in your 73rd year, you may decide to wait until the next year so your income tax rate is lower. And vice versa: If you have a liquidity event in your 74th year, you can take your RMD in your 73rd year instead.

A word of caution—if you choose to wait until the next calendar year to take your first RMD, you’ll have to receive another before the end of the same year. That’s double the distribution amount (and thus higher taxes owed) in one year.

Additionally, if you need more income than your RMD provides, consider drawing upon other income sources so you don’t jump to the next tax bracket. For instance, if your ordinary income rate is higher than the long-term capital gains rates, you may wish to generate income by selling appreciated long-term securities. Or consider ways to use tax losses from investments to offset gains and other income.

Eliminate your RMDs

Individuals who don’t need their RMDs can eliminate all or part of them by converting their retirement accounts to a Roth. Roth accounts don't pay tax on distributions—whether it’s a withdrawal of your contribution or the appreciation on your money. In other words, after contributing after-tax money, Roths can potentially grow tax-free for your entire life.

And, notably, there are no RMDs from your own Roth accounts. So that means when someone converts from a traditional to Roth IRA and pays tax on the converted amount (in the year of the switch), they’re done paying tax on those funds and any gains from those funds—FOREVER!

Let’s walk through hypothetical illustrations with two different goals.

Goal #1: Minimize taxes, no legacy

Devin and Sammy, a 64-year-old married Florida couple, just retired after selling their business for $1.6 million. They are working with their Wealth Advisor on a retirement budget. In addition to the proceeds from the sale, they have a $1.75 million traditional IRA. Here are the details of their plan. They:

Devin and Sammy, a 64-year-old married Florida couple, just retired after selling their business for $1.6 million. They are working with their Wealth Advisor on a retirement budget. In addition to the proceeds from the sale, they have a $1.75 million traditional IRA. Here are the details of their plan. They:

- feel confident they can live on $100K per year

- have enough money to cover this annual spend, so they don’t plan to take Social Security until age 70

- are not interested in leaving a legacy at this time

They asked their Advisor how they can reduce their taxes on their income from Social Security and their RMDs from their traditional IRA when they need to take them.

Their Advisor suggested a Roth conversion. Her analysis shows they should convert no more than 50% of the $1.75 million to a Roth, spreading the conversion over the next five years when their income tax rate should be lowest—a tax bracket trough—since they’ll have no other income until Social Security kicks in.

Calculations by Motley Fool Wealth Management. Married couple filing jointly. Total taxes paid is discounted at 2.5% to today's dollars through age 85. Maximum tax rate excludes tax rate on transfer to heirs. Assumes traditional IRA is invested in a balanced portfolio that delivers a market return of 5.38% from ages 63-70, then 4.72% return through age 85. Taxable income starting at age 70 from Social Security ($75,000 per year) excludes the 15% of Social Security not taxed. Past performance is not indication of future results. For illustrative purposes only.

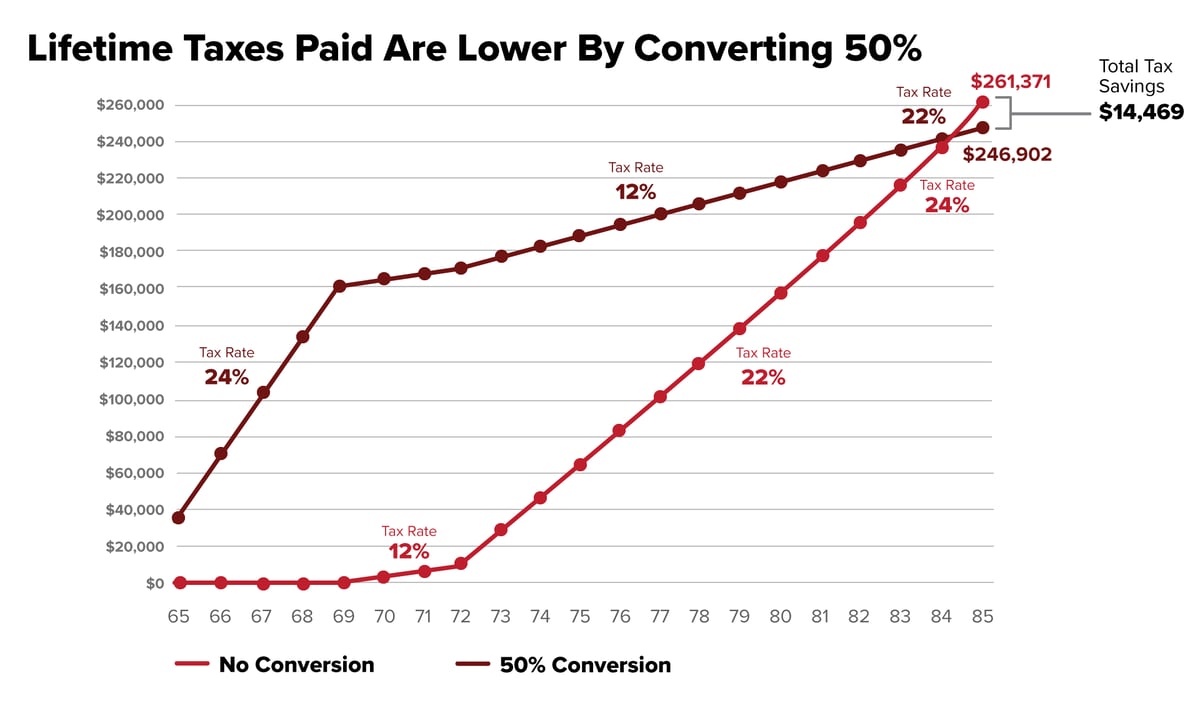

In both scenarios, Devin and Sammy pay taxes of $273,380 on the initial sale of the business (income of $1,600,000 less the standard deduction of $27,700 = $1,572,300). The differences start at age 65:

- No conversion: Over the next five years (ages 65-69), they have no income and pay no income tax. At age 70, their tax rate would only be 12% through age 73 when their RMDs kick in. From ages 73 through 82, their tax rate would be 22%, then kick up to 24% through age 85.

- Convert 50%: Over the next five years (ages 65-69), their income tax rate will be 24% on the amount they convert. Then it would fall to 12% through age 83. After that, it would go up to 22%.

When asked about converting more, the analysis shows that shifting more than 50% would generate higher taxes paid than not converting at all, which is contrary to their goal.

Goal #2: Minimize taxes, leave a legacy, and increase annual cash available

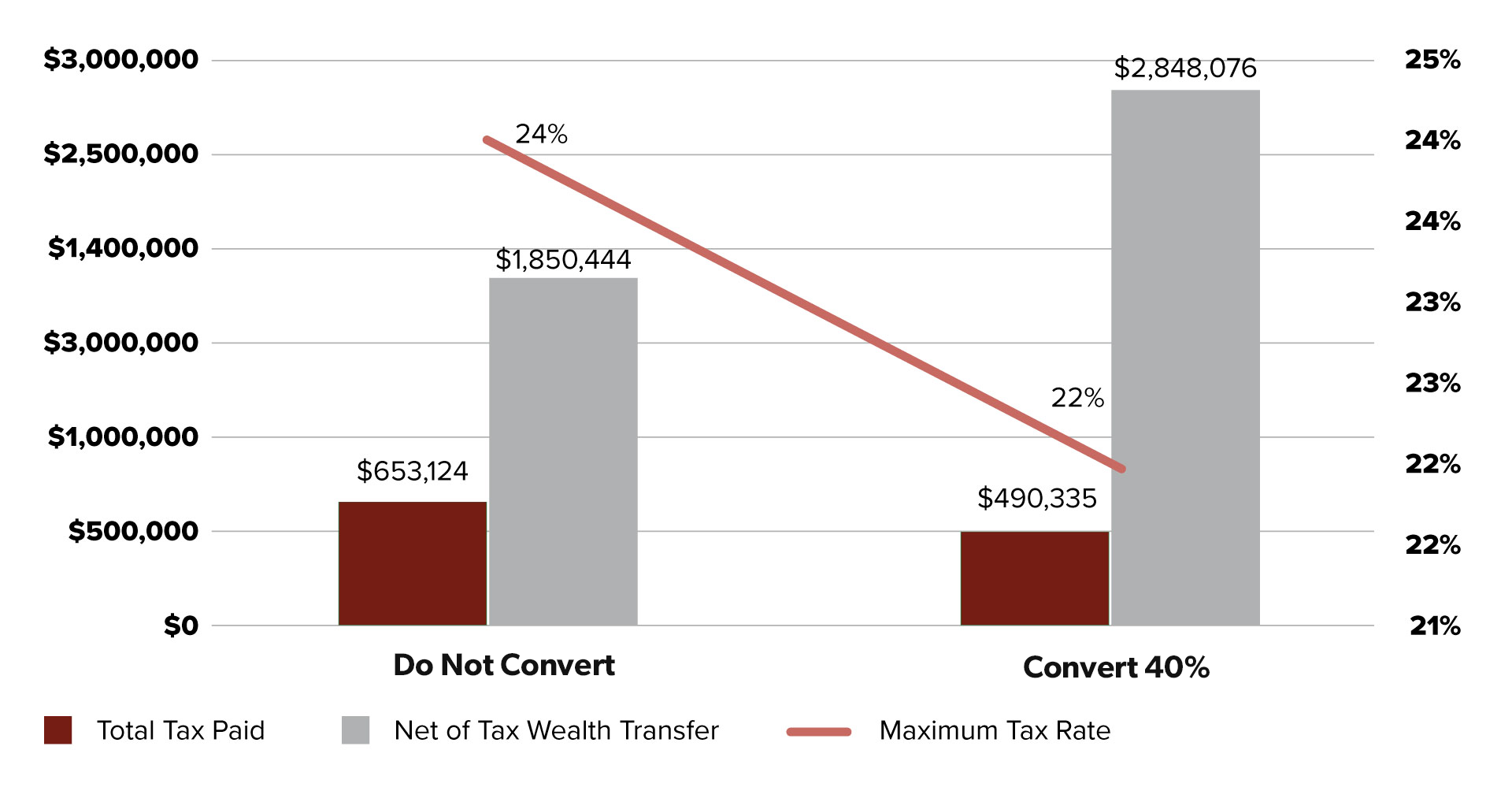

After careful consideration, Devin and Sammy decide they want to both lower their taxes and maximize the amount they can leave for heirs. But they’re also concerned about rising health care costs in their 80s and want to make sure they have at least $125K available each year during those years.

In this case, their Advisor suggested a 40% conversion. Like the 50% conversion, their taxes would be lower than not converting at all. In addition, Devin and Sammy would confidently have the desired $125K available each year in their 80s from their Social Security benefits and the non-converted portion (60%) of their RMDs without dipping into their Roth savings. (If they do not convert, they would also have sufficient funds to meet their desired $125K, but if they convert 50%, they would only have between $115K-$122K each year and may need to dip into their Roth savings.)

Finally, they would be able to leave nearly $1 million more—$2.85 million vs. $1.85 million—to their heirs than if they did not convert. And even more importantly, almost all—$2.1 million out of the $2.8 million—will be in a Roth, so their heirs likely will never have to pay taxes on the inherited amount. If they don’t convert, their heirs will need to withdraw the inherited IRA over 10 years (same time frame as a Roth) AND pay taxes on the full amount.

Do not convert vs. Convert 40%

Calculations by Motley Fool Wealth Management. *Discounted at 2.5% to today's dollars through age 85. Does not include a hypothetical/assumed 30% tax on inherited amount. **Excludes tax rate on transfer to heirs. Assumes traditional IRA is invested in a balanced portfolio that delivers a market return of 5.38% from ages 63-70, then 4.72% return through age 85. Past performance is not indication of future results. For illustrative purposes only.

Distribute your RMDs

Instead of donating cash or an appreciated security, you can give your RMDs from your retirement accounts to a cause you care about. This qualified charitable distribution (QCD) could make sense if you…

- would like to donate to charity during your life, or

- will not need your full RMD to support your living expenses, or

- do not have heirs, or do not prioritize leaving money to heirs.

QCDs are gifts to qualified public charities that, when done correctly, count toward your RMD each year. And more importantly, QCDs cancel out any tax you would have to pay on the RMD.

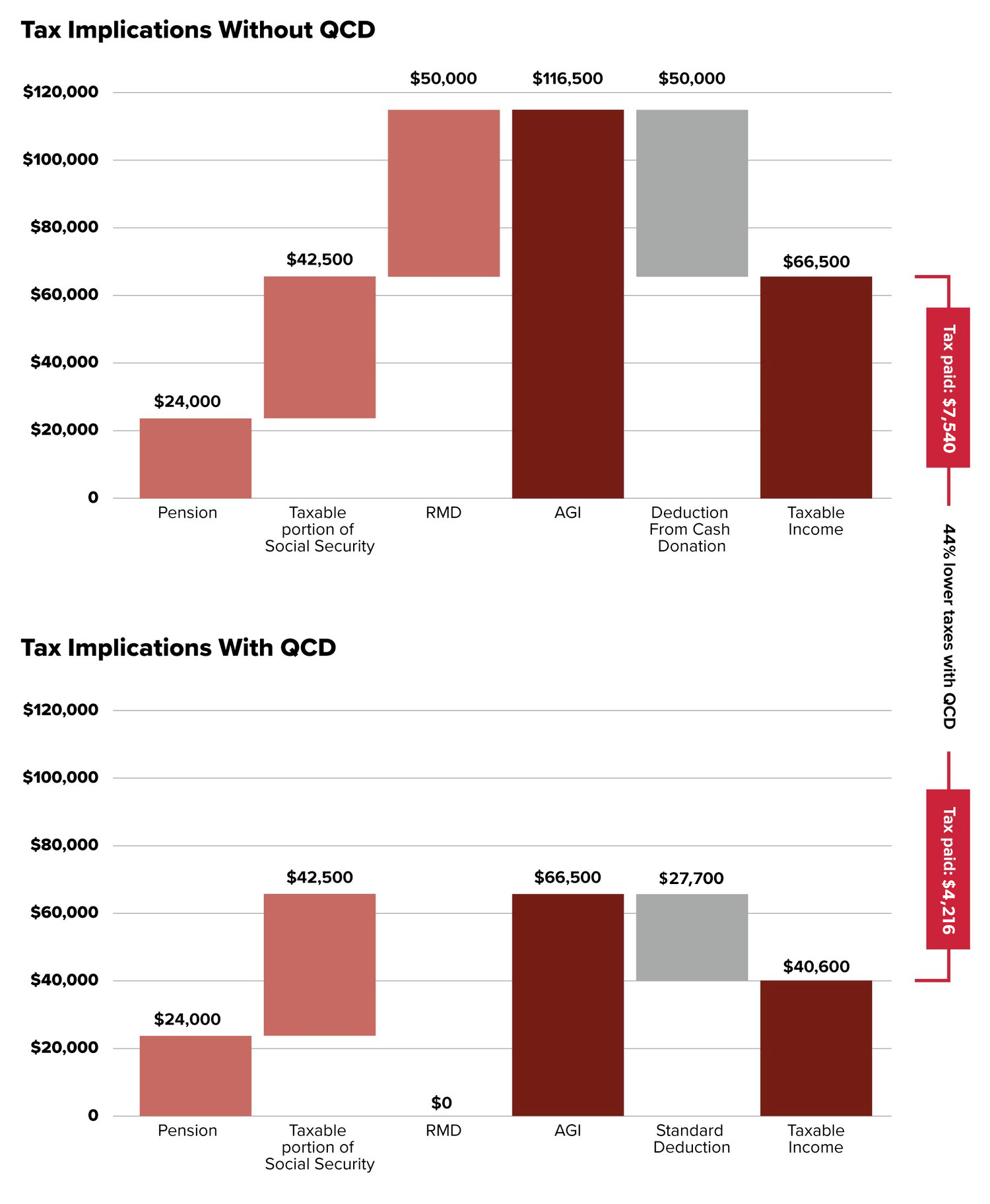

Let's take another example—Joe and Corinne, a retired couple weighing their options on making a $50K donation to their favorite charity. They planned on gifting cash, but their Wealth Advisor explained there could be a better way.

Let’s say they file their taxes jointly. They have a combined annual income of $24K from a pension, $50K in Social Security income (of which 85%, or $42,500, is taxable), and $50K of RMDs. Remember, RMDs are considered income and taxed at ordinary income rates.

Their Advisor computed two scenarios:

- Withdrawing their RMD, making a cash donation of $50K, and taking it as an itemized deduction on their tax return

- Making a QCD of $50K and taking a standard tax deduction

Here are the results of her analysis:

Source: Motley Fool Wealth Management. This analysis is hypothetical and for illustrative purposes only. For guidance and advice on taxes, consult your tax professional.

In both scenarios, Joe and Corinne gifted $50K to their favorite charity. But by making the QCD instead of a cash donation and taking the standard deduction, Joe and Corinne lowered their taxable income by the amount of the standard deduction, $27,700, resulting in paying $3,324 less in taxes—a 44% reduction.

There’s another important consideration: health care costs. (Yup, this again!) Making a QCD that reduces taxable income may mitigate exposure to Medicare Parts B and D income limits. In other words, the lower your income, the less you pay in Medicare premiums. So a potential benefit of making a QCD instead of taking an RMD is it may reduce the amount you pay for health care each year.

Of course, these decisions involve your individual tax situation, so always consult with your tax professional.

Tax on Investment Income

If you have a taxable brokerage account, then at some point you’ll probably want to sell some of your winners. And of course, you’ll get taxed on that investment gain.

So here are two savvy moves to lessen the blow.

Savvy Tax Move #2

Avoid Short-term Capital Gains

The first of the two moves is perhaps the simplest to implement, but at times could be emotionally challenging. Why is it an emotional decision? Because often, investors make up their minds to sell and want to do it right away. But long-term capital gains are preferable to short-term ones, AND you need to hold your investments for more than one year to avoid short-term capital gains.

Tax rates for long-term capital gains are 0%–20%, whereas short-term capital gains rates are 10%–37%, the same rate as ordinary income. For example, if you and your spouse have $500K in capital gains, you would much prefer to be taxed 15% than 35%!

Let’s walk through a hypothetical example to put this in perspective.

Let’s walk through a hypothetical example to put this in perspective.

Larry and June are considering selling two stocks. They've held Stock A for 11 months and Stock B for 13 months. They’ll recognize a $100K capital gain on each of them. How does their after-tax profit differ?

Short- vs. Long-term Gain Example

| Stock A | Stock B | |

|---|---|---|

| Holding Period | 11 months | 13 months |

| Initial Investment | $500,000 | $500,000 |

| Gain | $100,000 | $100,000 |

| Tax Bracket | 32% | 15% |

| Tax on Gain | $32,000 | $15,000 |

| After-tax profit | $68,000 | $85,000 |

| Annualized pre-tax return | 21.9% | 18.4% |

| Annualized after-tax return | 14.9% | 15.6% |

Difference in after-tax profit: $17,000

Source: Motley Fool Wealth Management. For illustrative purposes. Illustration is for a married couple filing jointly with annual income of $400K. Analysis ignores the net investment income tax, which would add a 3.8% charge on investment income in both scenarios.

By waiting just two months, (assuming that the capital gain is equal for illustrative purposes), Larry and June would keep an extra $17,000 of the investment profit. Said a different way, they would put 17% more of their profit in their pockets instead of paying it to the government!

Deductions and Credits

Eighty-seven percent of taxpayers take the standard deduction on their tax return, primarily because their home is either paid off, or other restrictions reduce the amount of write-offs available.5 But if you are able to itemize your deductions—with things like charitable donations, for instance—you may be able to push your tax bracket lower. For example, combined federal plus state tax rates can be upwards of 50% at the highest tax bracket. So if you can deduct your charitable gifts, every dollar you contribute to a charity could provide you a $0.50 tax benefit at that 50% tax bracket—a pretty good deal!

Conversely, the effective tax rate at the lowest bracket is roughly 10% (depending on state taxes), which means every dollar you contribute to a charity could provide you a $0.10 tax benefit—not as great a deal. So you see, it’s important to be mindful of how much you want to donate in order to lower your AGI, but to remain in the tax bracket that earns you the greatest benefit overall. HINT: It comes down to savvy moves #4, #5, and #6.

Savvy Tax Move #4

Bunch Cash Gifts

Let’s walk through a hypothetical example.

Sam and Veronica wish to make annual donations of 10% of their gross income— $27,500—to charity each year. Their Advisor suggested that bunching their gifts may make more sense. She ran the following analysis to show the impact.

Bunching Cash Gifts Example

| Scenario 1 | Scenario 2 | |||

|---|---|---|---|---|

| Year 1 Standard Deduction |

Year 2 Standard Deduction |

Year 1 $55,000 |

Year 2 Standard Deduction |

|

| Total Income | $275,000 | $275,000 | $275,000 | $275,000 |

| Charitable Contributions | ($27,500) | ($27,500) | ($55,000) | $0 |

| Applicable Deductions | ($27,700) | ($27,700) | ($55,000) | ($27,700) |

| Tax Paid | $46,152 | $46,152 | $39,600 | $46,152 |

| Taxes Paid Over Two Years | $92,304 | $85,752 | ||

| Effective Tax Rate Over Two Years* | 17% | 16% | ||

Tax Savings from Bunching: $6,552

Assumptions: Gross annual earnings for couple $275,000. Desired charitable contributions $27,500. Married filing jointly tax rate of 24%, graduated for income.

This example shows the potential benefits of lumping charitable gifts into one year rather than spreading them out over time.

In Scenario 1, Sam and Veronica’s annual donation of $27,500 was less than the standard deduction of $27,700. As such, they took the standard deduction on their tax return each year, resulting in a two-year effective tax rate of 17%.

In Scenario 1, Sam and Veronica’s annual donation of $27,500 was less than the standard deduction of $27,700. As such, they took the standard deduction on their tax return each year, resulting in a two-year effective tax rate of 17%.- Alternatively, in Scenario 2, Sam and Veronica’s gift of $55,000 exceeded the standard deduction in year 1, so they were able to write off the full amount on their taxes. In year 2, even though they did not make a charitable contribution, they were still able to take the standard deduction. Because of this bunching strategy, their two-year effective tax rate was 16%.

The result: While a 1% difference in tax rate seems minimal, Sam and Veronica saved $6,552 over the two years by bunching their gifts in one year. That's a 7.1% tax savings. And the charity still received the same amount, $55,000.

However, if they were concerned about the “lumpiness” of their gift, they could open and contribute the $55,000 to a donor-advised fund (DAF). That way, they could benefit from a lower effective tax rate (Scenario 2) and distribute the funds from the DAF annually—a win-win.

Savvy Tax Move #5

Give Appreciated Securities

There are also excellent tax advantages for giving noncash contributions, and the impact may be greater than a cash donation. In other words, when you have a security that has appreciated considerably over a holding period of one year or more, you can donate that security to a qualified charity and receive a charitable income tax deduction for the security’s fair market value. This means you can reduce your income and incur a lower tax bill as a result. In addition, when you donate an appreciated security, you can avoid the capital gains tax you otherwise would have to pay if you sold it for the gain.

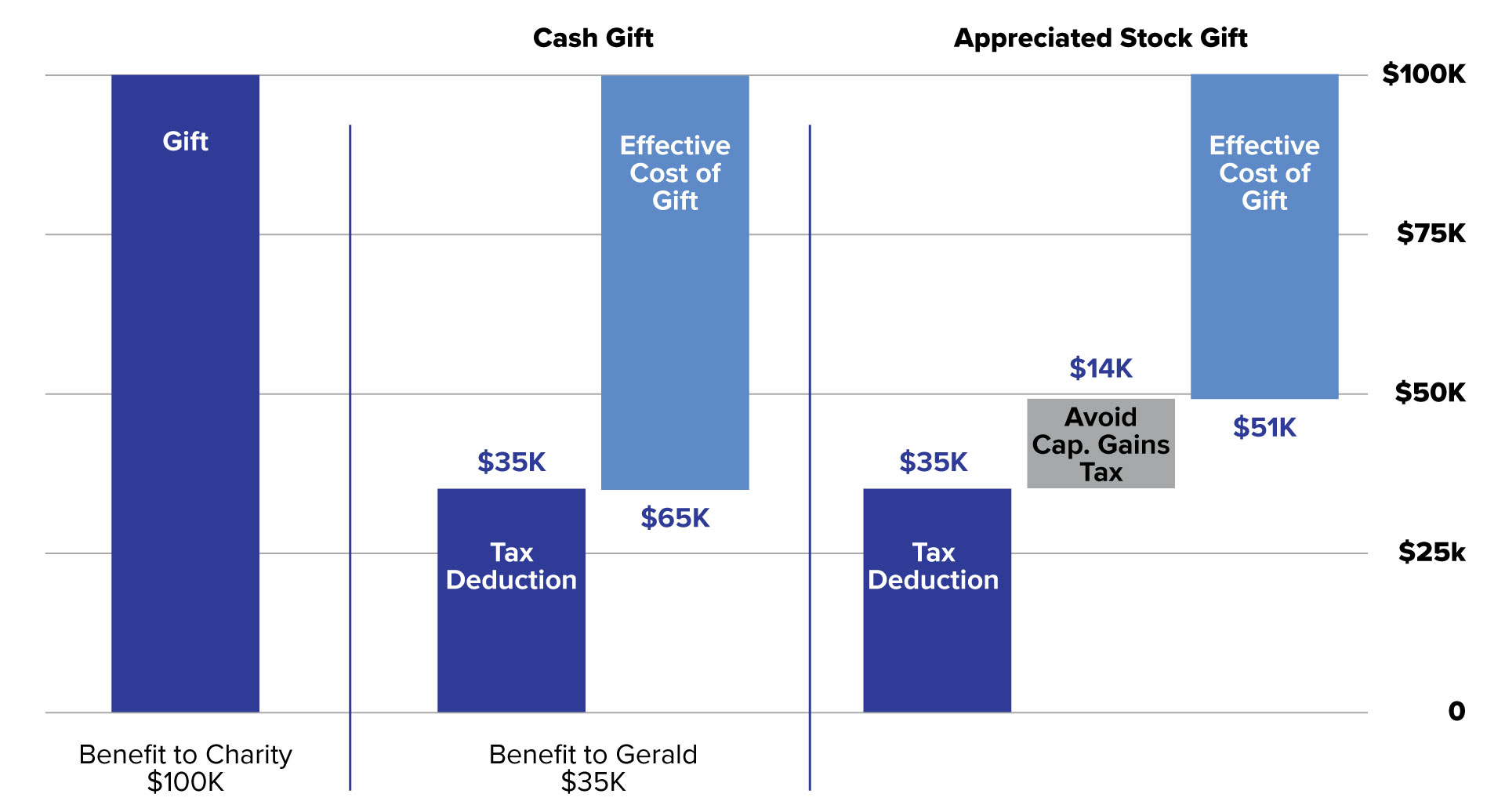

So how do you know if you should donate cash or an appreciated security? Gerald, in our next example, is facing this dilemma:

He would like to give to a charity in his mom’s name and is weighing the trade-off between gifting cash or an appreciated security. Here’s the analysis his Advisor showed him:

Tax Benefit of Cash vs. Stock Gift

For illustrative purposes only. Gift to qualified public charity. Federal tax rate: 35%. Long-term capital gains rate: 20%. Stock basis: 30%.

If Gerald makes a $100,000 cash donation, it could result in a charitable tax benefit of $35,000, effectively lowering the cost of the gift to $65,000. But by donating a security, Gerald can take the charitable tax deduction ($35,000) plus the benefit of not having to pay tax on the stock’s appreciation ($14,000), for a total effective gift cost of ($51,000). And if Gerald still wanted to hold that security in his portfolio—because he transferred and did not sell it—he can use the $100,000 of cash he has set aside for a cash donation and repurchase the security immediately, thus resetting his cost basis.

Legacy Planning

Savvy Tax Move #9

Two-For-One

What about a planning tool that combines income needs with legacy?

A charitable gift annuity (CGA) can do just that, by killing two birds with one stone so to speak. A CGA provides lifetime income and charitable giving. It works like this:

A charitable gift annuity is a contract between you, the donor, and a charity. After you make a sizable gift to charity—in the form of cash, securities, or another acceptable asset—you receive a fixed stream of income from the charity for the rest of your life. Once you pass, the remainder of the gift goes to the charity. In addition, you receive a tax deduction for the estimated portion of the gift that will eventually go to the charity.

A similar option is a charitable remainder trust (CRT). Like a CGA, CRTs provide income during your life, but instead of the charity being responsible for annual distributions, the trustee is responsible. CRT's are irrevocable trusts—meaning once the gifts are made and assets transferred, they are owned by the trust not the person. Payments from a charitable remainder trust to the donor are taxable and must be reported as income or capital gains. The donor also gets a tax deduction that is limited to the present value of the charitable organization's remainder interest. This is calculated as the value of the donated property minus the present value of the annuity.7

How do you know if you should use a CRT or a CGA? A CRT can be more appropriate than a CGA for folks that want to leave money to a smaller charity, or who want to have greater control around the underlying investment selections and payouts (options are unitrust where payouts fluctuate with actual income generated, or annuity where the payout amount is consistent over time).