To print this report or save it as a PDF, click here.

The term “Roth conversion” is just about as jargon-y as you can get. But for folks who might see retirement on the horizon sometime soon, it can be a powerful planning tool for optimizing existing retirement resources.

It’s not uncommon for dutiful savers to stash away the maximum contribution in their 401(k), 403(b), or IRA for decades. While growing substantial retirement savings isn’t a problem in and of itself, having a large portion of your future retirement income be subject to required minimum distributions (RMDs) and ordinary income tax is. See, the taxman always comes knocking—and a Roth conversion can put you in greater control of when and how much to hand over at any given time.

Just as you can be strategic with timing your Social Security benefits or other retirement resources, Roth conversions are powerful planning tools for proactively reducing RMDs and creating potentially tax-free income to enjoy in retirement. As we’ll dive into more detail below, some people can even save on their lifelong tax liability by opting for a multi-year Roth conversion strategy before retirement—though this depends on quite a few factors.

Ready to learn whether a Roth conversion is right for you? Don’t worry, we’ve covered every question, tip, trick, and must-know in this in-depth guide.

Common Retirement Accounts (And How They’re Taxed)

Why Do a Roth Conversion?

A Roth conversion enables your retirement savings to reap some of the benefits of both a traditional IRA or 401(k) and a Roth account.

When you first contributed to your 401(k), you were able to deduct those contributions from your taxable income for the year. Considering how high the annual contribution limit is for 401(k)s, this benefit can yield immediate and sizable tax savings. Over time, those contributions grow tax-deferred—allowing more of your wealth to compound without interference.

But as retirement approaches, or as your annual income levels evolve, you might want to take action now to secure tax-free income in retirement. A Roth conversion allows you to convert as much or as little of your existing pre-tax resources into future tax-free income. In years when your other income sources are low, for example, it might make sense to complete a bigger Roth conversion.

Another benefit of converting funds from your 401(k) or IRA into a Roth account? A Roth account does not have required minimum distributions (RMDs) since the IRS already received its cut of your contributions. You can allow the funds to sit and grow for your entire life (and potentially the life of your spouse as well), without having to strategize and plan for required withdrawals in retirement.

In addition to these important benefits lie several critical advantages worth a closer look.

Lowering your future tax bracket on other income. |

|

|

Assuming you’re able to take qualified withdrawals in retirement, what you pull from your Roth account won’t increase your taxable income. For this reason, Roth withdrawals can be powerful tools for minimizing your total tax liability by keeping your tax bracket lower for other income that does get taxed at the ordinary income tax rate (like traditional 401(k), IRA distributions, and a portion of Social Security) |

Taking advantage of low-income years. |

|

|

Your income will fluctuate throughout your lifetime—and it’s not guaranteed to always go up and up and up. You may need to take time off work to care for an aging parent, raise a child, focus on higher education, or otherwise reprioritize your time. You could also be laid off work during an economic downturn, earn lower-than-usual commissions, or quit a steady job to start building a business. In the years when your taxable income is lower, it’s safe to assume your tax bracket will likely be lower as well. If you have the funds to cover the tax liability of a Roth conversion, this could be an effective way to do the conversion while paying less taxes on it—especially if you anticipate your income rising again in the future. Many retirees encounter a natural lull in their income in the years after they stop working, but before claiming Social Security, pensions, and starting to collect those pesky RMD’s. While it can sound appealing to lock in an artificially low tax bill in those years, our job as wealth advisors is to consider your lifetime tax liability, not just optimizing single years. This is where a change in the status quo can set the stage for longer-term planning via Roth conversions. |

Reducing Medicare premiums. |

|

|

You may be required to pay more than the standard base for your Medicare Part B and Part D based on your modified adjusted gross income (MAGI). This additional premium is called the “income-related monthly adjustment amount (IRMAA),” and it means you could be responsible for paying up to 85% of your Medicare monthly premium, as opposed to the standard 25%.7 In 2025, for example, the portion of the standard Part B premium plan participants are responsible for paying is $185 per month. But if your latest tax return shows a MAGI above $106,000 (or $212,000 for married filers), you’ll have to pay more.7 (When dealing in government time, “latest tax return” means your tax filing from 2 years ago. Therefore Medicare would be looking at your 2024 tax return to estimate your 2026 Medicare premium.) Because withdrawals from a Roth account don’t add to your taxable income, they won’t increase your MAGI. Balancing your other taxable income with Roth distributions can help optimize your MAGI each year in retirement to keep those additional Medicare premiums in check. |

The Value of Roth Accounts in Legacy Planning

While you may be considering a Roth conversion for your own potential tax savings, think even more broadly. When done effectively, a Roth conversion can help minimize your lifetime taxes as a family unit—meaning the benefits impact not only you, but your spouse and children (or other beneficiaries) as well.

We’ve established that Roth accounts don’t have RMDs. You have the freedom to continue contributing to your Roth account throughout your lifetime, and you never have to take a dime out of it if you really don’t want to.

Many retirees like the idea of using their Roth account as a way of leaving surplus retirement savings to their heirs. Similar to the rules for the original account owner, withdrawals of the original contributions are tax-free, and earnings may be withdrawn tax-free as well as long as your beneficiaries meet the requirements. Namely, the account needs to be older than five years before tax-free withdrawals can be made.8

It’s important to note here that an inherited Roth IRA will likley be subject to the 10-year rule, meaning the account must be emptied within 10 years of the original owner’s death. However, certain eligible designated beneficiaries (including a spouse or minor child) are not held to this requirement.8

When legacy planning is a priority, it’s critical to work with your wealth advisor and estate planning professional to determine appropriate beneficiaries in order to maximize the tax-free compounding potential of a Roth IRA. Let’s look at an example:

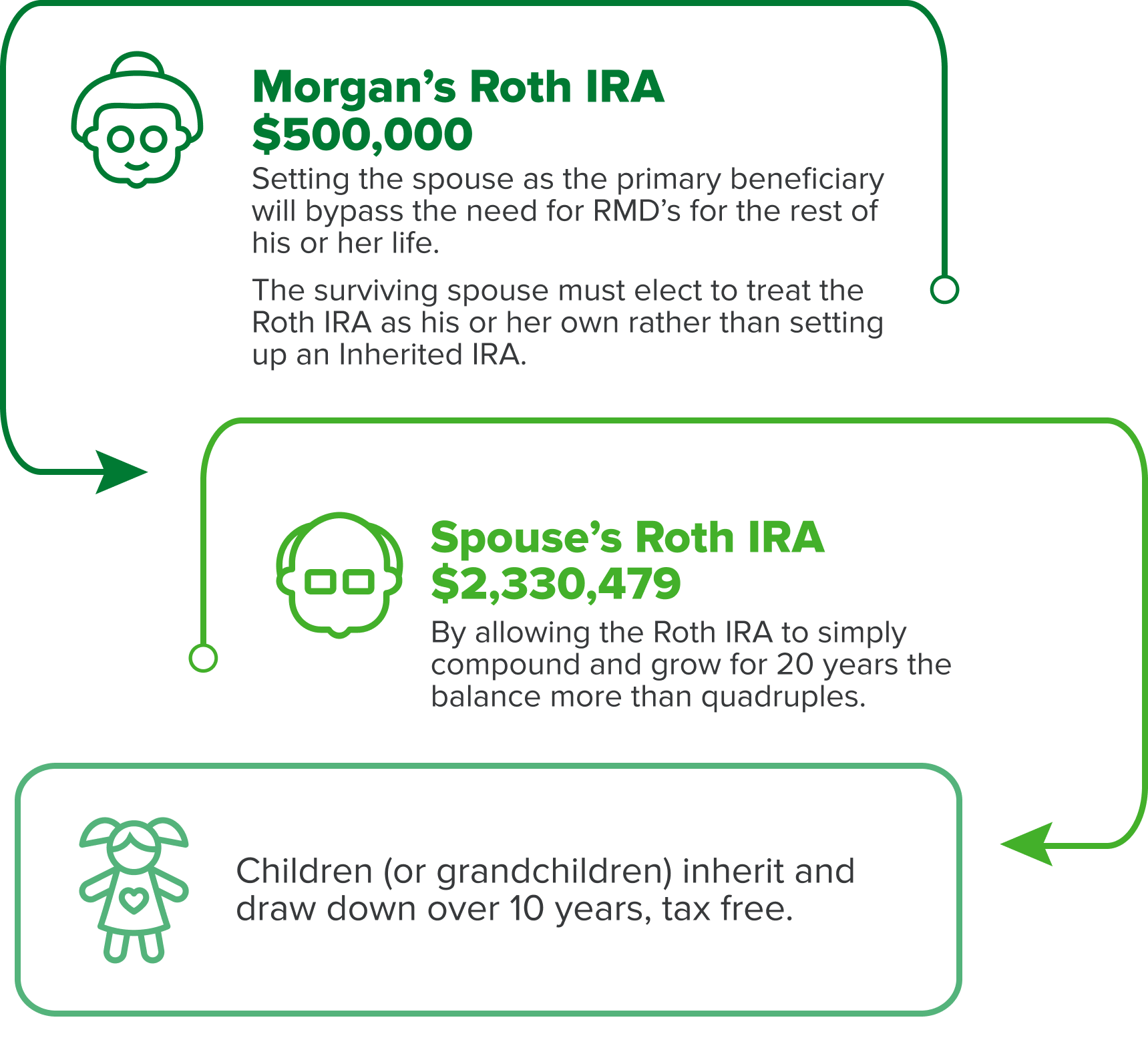

After careful planning and Roth conversions over the years, Morgan has accumulated $500,000 in a Roth IRA at age 70. Let’s assume an 8% rate of return on the Roth investments.

|

If Morgan establishes his or her spouse (who is the same age) as the primary beneficiary of the Roth IRA, the spouse will benefit from a special rule that permits the spouse to skip RMD’s during his or her lifetime as well. After an actuarially impressive 20 years, Morgan’s spouse bequeaths the IRA (which has now reached over $2.3 million) to their children who will have 10 additional years of tax-free growth after considering their annual RMD withdrawals. |

|

Now let’s assume the same facts, except Morgan didn’t consult with a wealth advisor. He or she was so excited to pass wealth to kids and grandkids, all of whom are over 21 years old. Those beneficiaries will have to immediately start taking required minimum distributions, and have lost the power of earning 1.8 million extra tax-free dollars. |

This might feel like an extreme example, but it illustrates the importance of having a knowledgeable advisor to help each step of the way. One might think that the decisions to complete a Roth conversion, of what value, and in which year(s) would be the hardest part. However, these accounts will likely have a life beyond your own to consider, and can have a big impact on the net-of-tax wealth you are able to share.

Why Not Do a Roth Conversion?

Is a Roth Conversion Right For Me?

Case Studies

How Do I Do a Roth Conversion?

7 Things to Know

In this section, we’ve rounded up the “you should really know this” fast facts about Roth conversions. They very well could be the deciding factor for determining when or if a conversion is the right choice for addressing your retirement income needs.

You don’t get a do-over: |

|

|

Once a Roth conversion is complete, you cannot reverse it. In fact, the only other account you’re allowed to roll a Roth IRA into is another Roth IRA. You cannot transfer the funds back into a tax-deferred account, like a traditional IRA or 401(k). |

You could have a big tax bill: |

|

|

The amount of money you convert from a traditional retirement account into a Roth IRA is subject to ordinary income tax the year you convert. If you convert $50,000 in 2025, that will increase your taxable income by $50,000 when you file your tax return come next April. You’ll likely want to keep the funds intact in order to maximize your future retirement income (and potentially avoid a 10% early withdrawal penalty), which means you’ll need to use other means to cover the tax bill (like cash reserves). You may be able to liquidate some of your taxable brokerage account, though this could disrupt your portfolio’s growth path and incur more tax liability along the way. |

Conversions are commonly spread out over several years |

|

|

The purpose of a Roth conversion is to help reduce your lifetime tax liability. To do this, you need to be strategic about when and how much you convert each year. Most people tend to spread out their Roth conversion across several years (even decades) in order to keep their taxable income at a reasonable tax rate. For example, a one-time $1 million conversion will jump you up to the highest tax bracket (37%) and create a significant tax liability—one you may not be able to cover out of pocket. By breaking it down into more manageable, bite-size conversions annually, you can keep your tax rate the same (or only slightly elevated) while still ensuring the future benefits of tax-free retirement income. |

Your rollover could come as cash or investments: |

|

|

If you’re converting a traditional IRA, most of the investments that already exist in the account can be converted directly to a Roth IRA without interference. But if you’re converting a 401(k) into a Roth IRA, you’ll typically receive a check for the cashout value of your account. You’ll need to deposit the check into the Roth IRA and then select investments you wish to purchase. |

Your traditional 401(k) or IRA value is based on market price: |

|

|

You’ll receive the closing market price on the day your conversion is processed. This is what your tax bill will be based on, and how much you’ll receive either as a payout check or IRA rollover. |

You can’t skip your RMDs: |

|

|

If you choose to do a Roth conversion after your RMDs have already started, you must take any required distributions from your IRA or 401(k) for the year before converting the account. Remember, RMDs are also subject to ordinary income tax and will need to be considered alongside the rest of the Roth conversion tax liability. |

Going “all in” on Roth can be a devil’s bargain: |

|

|

If you’re thinking about riding the Roth conversion highway to a lifetime of tax-free income, you may be cutting off your nose to spite your face. Because of the progressive tax system in the United States, age-based benefits for the older and wiser population, and potential state level tax benefits, it can be very attractive to have some un-converted pre-tax savings to draw down at bargain rates in your elder years. |

How Can I Keep Adding to the Roth?