Employer-Sponsored Retirement Accounts

Individual Retirement Accounts

Switching Among 401(k)s, Traditional IRAs, and Roth IRAs

There are also ways to shift assets from one type of account to another. For example, if you leave an employer, you may roll over your old 401(k) into your new 401(k) if allowed or to an IRA to consolidate your assets. Or you may contribute to a traditional IRA, then convert it to a Roth via a “backdoor” conversion. There are many advantages to doing these financial maneuvers, and we’ll cover each of them below.

- 401(k) rollover: Consolidate accounts and gain the opportunity for more customized investment choices and possibly lower costs.

- Partial conversion: You can convert all or part of an existing retirement account, such as a 401(k) or a traditional IRA, into a Roth IRA.

- Backdoor Roth: Transfer money from a traditional to a Roth.

Should you roll over your old 401(k)?

Have you transitioned to a new employer and left your 401(k) behind? Regardless if it has a few hundred or a few million dollars, you need to decide what to do with the funds. Unfortunately, many people don't know their options.

We’ve identified several potential solutions for managing 401(k) assets that remain in a former employer’s retirement plan.

Several factors may impact which choice might be best for you, including the investment lineup (what investments you can invest in), fees (administrative and other), and ease of keeping track of the assets (knowing where all your retirement assets are and how much they are worth).

So, consider each of these money moves:

- Keep it with the former employer. If you are comfortable with the investment options and are pleased with the performance and fees, it might make sense to keep your retirement account invested in your previous employer’s plan. Tax implications: None since funds remain in plan. However, some plans kick out participants with low balances.

- Rollover into an IRA. Many people choose to roll over their old 401(k) into an IRA in order to consolidate accounts into one investment account. Additionally, IRAs may offer broader investment choices and/or lower costs. Tax implications: Rollovers are tax-free.

- Rollover into a new employer's plan. Depending on your retirement plan’s rules, you may be able to roll over your old 401(k) into your current employer’s plan. This will consolidate the assets and consistently invest them with your current asset allocation. Tax implications: Rollovers are tax-free.

- Cash out. Some individuals decide to withdraw their retirement savings altogether. But if you cash out before age 59½, you will have to pay taxes on your entire withdrawal. In addition, the IRS takes out 20% withholding for taxes and a 10% early withdrawal penalty when you file your tax return. These fees and penalties can drastically reduce your savings. For these reasons, the cash-out strategy is generally the least favorable option. Tax implications: Heavily taxed and penalized.

So, which solution is best for you? Although individual circumstances differ, the benefits of rolling over a 401(k) to an IRA can often typically outweigh the other options for many people. Here’s why.

Benefits of rolling over your 401(k)

Today, the rollover process has become more streamlined and simplified. While this simplicity is a bonus, there are five distinct advantages to an IRA rollover.

Advantage No. 1: Greater investment choice and account mobility.

Depending on your former employer’s retirement plan, your old 401(k) asset allocation may not have kept up with the times. For example, many old plans had limited investment options. Others may have locked you into so-called low-risk “stable” options as defaults.

Now is your opportunity to hit the reset button and create an investment portfolio that is more in line with your current financial objectives. It’s your chance to customize your own retirement plan. And because your IRA won't be connected to your employer, you may have more flexibility, privacy, and control, so you can change jobs with less worry.

Advantage No. 2: Lower costs.

High fees also weigh down some older plans. Unfortunately, these fees—to invest, withdraw money, take a loan, and for recordkeeping and printed statements—are often passed on to retirement plan participants like you.

Some of these account fees may still exist today. But many have vanished, in part because there's more transparency, and it’s much easier to track charged fees.

Advantage No. 3: Consolidation.

Keeping up-to-date on various isolated accounts is not easy—especially as individuals age and life gets busier and more complex. Consolidating retirement accounts can make tracking assets more convenient. But it's more than that. Bringing together retirement assets in one place also can help you visualize where you are in your retirement plan and how far you need to go. It can paint a more complete investment picture of your total asset allocation, risk exposure, and overall return.

Advantage No. 4: No taxes or penalties with a direct 401(k) rollover.

Participants can move money from one retirement account to another without penalty. This is known as a direct rollover. But don’t make the mistake of having your old company cut a check payable to you. This is considered a distribution and means your 401(k) plan is required to withhold 20% for taxes.

Advantage No. 5: More options for early withdrawals.

Although taxes will be owed, IRAs allow early distributions without penalty for certain expenses, like higher education and first-time home purchases. Conversely, the 10% tax on early withdrawals from a 401(k) is waived in only a few severe circumstances, like total disability or medical bills that exceed 10% of adjusted gross income. But unlike with a 401(k), you can’t borrow against an IRA.

When should retirement assets stay inside an employer plan?

A rollover may not be the right decision for your situation despite the benefits. There are several reasons why keeping assets in a current 401(k) may make more sense.

| Creditor Protection | 401(k)s generally provide better protection against bankruptcy and claims from creditors. | |

| Loans | Loans from IRAs are not allowed, decreasing financial flexibility in times of need. | |

| Working Longer | If you work past age 73, you do not have to take required minimum distributions (RMDs) from your 401(k). But an IRA would still mandate annual distributions. | |

| Early Retirement | Want to retire early and need income? Individuals can start taking qualified distributions from a 401(k) at age 55, slightly earlier than allowed with an IRA. | |

| Company Stock | Does your 401(k) hold company stock? Unfortunately, transferring it to an IRA may not offer the most favorable tax treatment. Instead, you could move the company stock to a taxable brokerage account in a maneuver called Net Unrealized Appreciation. That way, the gains are only subject to capital gains tax, which is usually lower than income tax. (Net Unrealized Appreciation is a limited time opportunity, so consult with a wealth advisor as soon as you separate if you hold employer stock in your plan.) | |

| Roth Strategies | Completing annual "backdoor" Roth conversions may be tax-efficient for you. (More on this strategy in a moment! And, another excellent topic for you to discuss with your qualified tax advisor!) | |

Refine your retirement strategy under one roof

Saving for retirement seems like a simple concept. But managing a retirement strategy is complex.

It's made even more complicated when assets are spread among various accounts managed independently—with differing and sometimes competing objectives or goals that made sense 30 years ago but may no longer seem appropriate near retirement or in an evolved investment environment.

A noncentralized approach can make selecting an appropriate asset allocation and risk level overwhelming, even for the most financially astute.

Case in point: Harry Markowitz, the 1990 Nobel Prize in Economics recipient. Known as the father of Modern Portfolio Theory, Markowitz's research on the efficient trade-off between risk and return underpins most asset allocation models. Still, he famously split his portfolio evenly between stocks and bonds in the 1950s. But Markowitz recognized that what worked in 1952 may not work today, explaining he now divides his money "among asset classes, like efficient portfolios…"

This example illustrates the importance of refining investment strategy and asset allocation. Because what worked in the past may not work now. But it’s hard to know where you stand when retirement assets are all over the place.

Fortunately, rolling over an old 401(k) can be simple and easy. Here’s how to get started:

Source: Motley Fool Wealth Management

So, “rolling over your 401(k)” is just a fun way of saying that you’re going to move your money from a 401(k) account to a different kind of retirement account, such as an IRA. There are a few of these kinds of money movements you can make among retirement accounts.

Enter the "IRA Conversion"

A Roth IRA conversion is when you take all or part of your existing traditional IRA or 401(k) and move it into a Roth IRA.

As we discussed earlier, there is the distinct advantage of not having to pay taxes on withdrawals from a Roth IRA, and so we often hear something along the lines of, "I want to avoid paying taxes, so I'm going to move all my IRA money into a Roth IRA.”

For some people, this move may make perfect sense. But for others, it may not.

The crux of the issue is tax optimization: Which is better—small tax payments over time (via traditional periodic distributions) or one large tax payment immediately (Roth conversion)?

What’s the breakeven?

Taxpayers can convert a traditional IRA into a Roth, even if they’ve started taking their required minimum distributions. However, a taxpayer cannot change over just the annual RMD into a Roth.

One way to assess whether a Roth or traditional IRA could be best suited for your situation is to look at a breakeven analysis, which examines the point at which profit and loss are equal.

Consider the following hypothetical example:

David and Janice, both in their mid-70s, were contemplating moving $2 million from their traditional IRA assets into a Roth. The reason was simple: Their RMDs from a traditional IRA exceed their living expenses. In addition, by having a higher income, they may be subjected to increased Medicare premiums or a higher hurdle for deducting medical expenses on their tax returns.

But by moving their assets to a Roth, they would not be required to take—or pay taxes on—distributions they did not need.

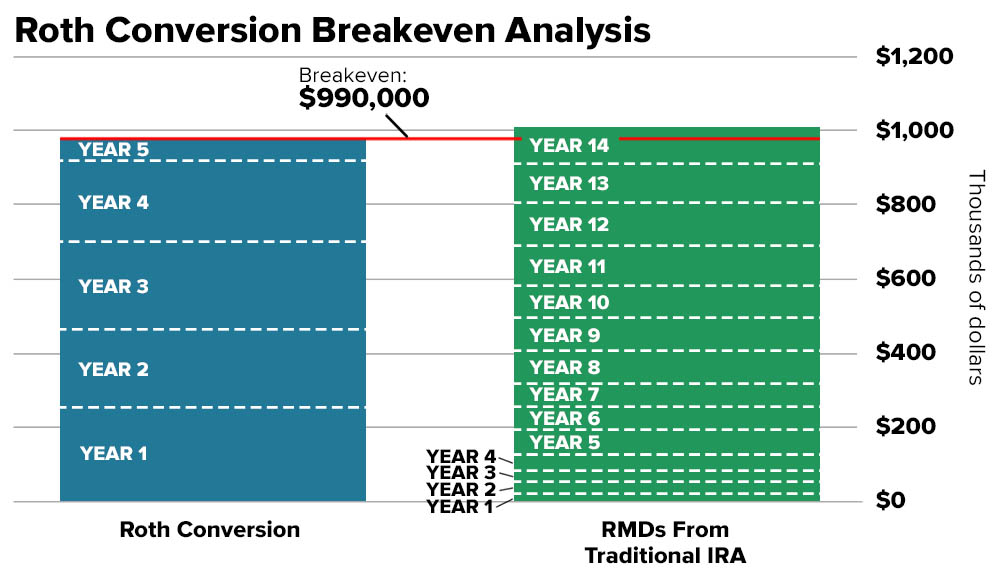

Their Fool Wealth planner performed a breakeven analysis based on a five-year conversion plan. Notably, leaving a legacy was not a priority for them. The results were as follows:

What does this chart tell us? First recall that the money David and Janice put in their traditional IRA was not taxed.

So when they convert funds from their traditional IRA to a Roth IRA, they will have to pay taxes immediately on the amount shifted into a Roth.

That is what the blue bars show. So in Year 1, they would pay taxes of $246,481 based on a 35% tax rate.

Now, compare that to the tax bill on their RMDs if they keep the money in their traditional IRA (green bars).

Because their annual RMD is lower than the amount converted into a Roth, and their tax rate is based on their applicable marginal rate, the tax bill each year is lower than the Roth conversion. For example, in Year 1, they would pay $19,881 in taxes.

So should they convert to a Roth? The analysis shows that David and Janice's breakeven for a Roth conversion would be 14 years.

Said a different way, it would take them 14 years for the amount paid in taxes on their annual RMDs to equal the amount paid in the Roth conversion.

So each would be well into their 80s before the switch made tax sense. And because they were not interested in leaving money to heirs, a Roth conversion did not make sense for them.

Converting via the "Backdoor"

"Backdoor" Roth conversions have been widely touted as a "rich person's Roth." That's because if your income exceeds the maximum limit to contribute to a Roth directly, you can take the indirect route of adding the annual maximum amount to a traditional IRA and then immediately transferring that contribution to a Roth account. Many wealthy Americans have reportedly socked away a pretty penny this way.

Is this a scheme to dodge taxes?

Yes and no. Yes, a backdoor Roth strategy will decrease the taxes you pay over your lifetime, but it is also perfectly legal. Investors have to pay a tax on all non-taxable money that moves from a traditional to a Roth in the transition year.

While this strategy is legitimate, it has nonetheless drawn lawmakers' focus. However, at this point, the backdoor Roth still lives on.

What are the advantages of building your Roth IRA?

The benefits of this financial maneuver to increase your Roth assets can be numerous. For instance, as we mentioned earlier, all earnings in a Roth IRA grow and are withdrawn tax-free.

In addition, Roths do not require RMDs. This means assets can continue to compound tax-free for the rest of your life and beyond. That's why many may view this type of account as an excellent way to transfer funds to heirs.

As with everything related to estate planning, leaving your Roth IRA to heirs has its own set of rules. The basic gist is:

- Spouses who inherit a Roth IRA can treat it as their account and are not required to draw down the account during their lifetime.

- Particular specially classified beneficiaries who inherit a Roth IRA maintain the "stretch" distribution schedule throughout their lives.

- Other non-spouse beneficiaries—such as children, grandchildren, other family members, and friends—must take distributions of all the assets in the account within 10 years of the original owner's death.

There are other rules, so consult a tax professional for all tax advice.

But not everyone is a good candidate for a backdoor Roth...

For example, if you already have before-tax contributions held in a traditional IRA, converting to a Roth may not be tax-efficient.

The reason is complicated, but if your IRA consists mainly of pre-tax contributions and you have significant accumulated earnings, most of the funds you convert to a Roth IRA will likely count as taxable income at the time of the conversion.

You aren't allowed to "cherry-pick" and only transfer the after-tax balance, which could kick you into a higher tax bracket in that year. If that's the case, it may make sense to wait until retirement, when you'll likely be in a lower tax bracket.

But start with a fresh slate. Even though your contributions will be taxed immediately, you won't have to pay taxes on earnings—which is one of the advantages of backdooring into a Roth.

Contrast that with socking away the same amount in a taxable investment portfolio. Similarly, your investment dollars will be taxed immediately. But they're also taxed when you sell appreciated positions.

Let’s walk through an example

Larry recently graduated college and is saving $6,000 a year over and above his employer's 401(k) contributions.

However, Larry's income is over the limit for contributing directly to a Roth IRA, so he thought the Roth just wasn't in the cards. That is until his colleague mentioned that he might be better off doing a backdoor Roth instead.

So he decided to speak with a financial advisor to understand his options. Here's the analysis the advisor reviewed with Larry.

Larry’s advisor assumed he would make an annual contribution of $6,000 for the next 30 years. In addition, the advisor based the growth of the investments on the long-term average return of 8.29% of a 50% stock/50% bond portfolio5.

| If in a taxable brokerage account | |

|---|---|

| Accumulated Balance: | $499,699 |

| Taxable Account Tax Rate:Assuming 15% Federal + 5% State | 20% |

| After-Tax Value: | $579,759 |

| If in a Roth | |

|---|---|

| Accumulated Balance: | $499,699 |

| Roth Account Tax Rate: | 0% |

| After-Tax Value: | $679,759 |

| Tax benefit of a Roth over a taxable account | $100,000 |

|---|

This example shows the potential tax advantage—$100,000 in this example—of the backdoor Roth over a taxable investment account. And while Larry was embarking on his career, those well into their careers may also see substantial benefits.

What's your "why" for doing a backdoor Roth?

While converting to a Roth appears to be the financial move du jour, the decision should be highly individualized. Larry's decision should weigh other factors—such as his wealth goals—and the after-tax value.

For example, does he want to spend his contributions before 59½ years old? If so, then a Roth could make sense. But if he needs to dip into the earnings, he may get penalized and taxed.

Something else to mull over? Managing your future tax bracket.

The backdoor Roth is an effective technique for controlling future overall tax rates. In other words, by drawing spending needs from this tax-free bucket in retirement, your taxable annual income will not increase.

Thus, your tax bracket should be unaffected. In contrast, spending from a taxable investment account or a traditional IRA could raise your tax bracket.

But as with everything, there are other pros and cons. That's why it's essential to look at it from all angles. Again, a financial planner and tax professional can help guide your decision.

Choosing a Retirement Account is Not Necessarily Mutually Exclusive

We just spent a lot of time explaining the similarities and differences among the various retirement savings accounts. But in practice, they're not mutually exclusive. You can potentially invest in all three at the same time.

But if you do, the available tax benefit may be lower or unavailable in the year you make the contribution. And whether you have just one or multiple IRAs, your total annual contribution is still capped at $6,500 ($7,500 over age 50). There are other rules, so consult with a tax professional to understand the impact on your situation.

In general, we believe you should start with a 401(k) if one is available to you. And if you are able, max out your contributions and take advantage of any company match program. Then consider an IRA.

Not sure which makes sense for you? This chart may help.

But consider this: the optimal solution may be a mix of both.

That way, individuals could take deductions at the highest tax bracket while working and recognize income in the lowest tax bracket in retirement. This tax-arbitrage strategy is lost if 100% of assets are in only one approach.

Source: Motley Fool Wealth Management

You've Saved. Now It's Time to Withdraw